Decisions regarding new product investments are among the most significant a firm’s management makes. These decisions shape the company’s strategic direction, allocate limited resources, and communicate priorities to both employees and investors. However, the process for making these product investment decisions can differ greatly among firms. For instance, a mid-sized company might consider various approaches in terms of decision authority: should a single leader decide, should the top management team share the responsibility, should senior managers collaborate in deliberations, or should all members of the leadership team have an equal say?

Research across economics, management, political science, and psychology suggests that the size of the decision-making group fundamentally alter how decisions are made, which problems arise, and what trade-offs become unavoidable. This text compares four distinct cases for a hypothetical mid-sized firm revising its product investment process:

- Single decision maker (e.g. the CEO decides).

- Five top executives (the C-suite collectively decides).

- Twenty senior executives (executives and VPs decide jointly).

- One hundred leaders (80 directors plus 20 executives, all with equal rights).

By analyzing these four scenarios side by side, we can see how the challenges of coordination, information processing, incentives, conflict management, and legitimacy shift as groups grow larger.

This text is part of the series on decision governance. Decision Governance is concerned with how to improve the quality of decisions by changing the context, process, data, and tools (including AI) used to make decisions. Understanding decision governance empowers decision makers and decision stakeholders to improve how they make decisions with others. Start with “What is Decision Governance?” and find all texts on decision governance here.

Case 1: One Decision Maker

When the CEO alone selects new product investments, the process is streamlined. Business units submit proposals, the CEO—perhaps with help from staff in strategy and finance—reviews them, and a decision follows swiftly.

Advantages are obvious. The process is fast, consistent, and aligned with what the CEO aims for. There is no ambiguity about who is accountable. This is especially valuable in turbulent markets where speed is critical.

But risks are equally clear. Decisions reflect one individual’s knowledge, biases, and cognitive limitations. Blind spots are inevitable. Behavioral economics has shown how individuals systematically deviate from rationality—through overconfidence, anchoring, or loss aversion. Concentrating decisions in one person magnifies these biases. Legitimacy is also fragile: managers whose proposals are rejected may feel excluded, and the process may appear arbitrary.

In governance terms, this model requires little process infrastructure, but it is brittle. It works best when the CEO is unusually capable, when the environment demands rapid response, and when the firm is small enough that unilateral decisions can still be effectively implemented.

Case 2: Five Top Executives

When the C-suite of five executives decides jointly, the process gains balance relative to Case 1. Proposals are prepared and pre-screened, then reviewed in meetings where each executive brings a functional perspective—finance, operations, marketing, R&D, HR.

The advantages are diversity and deliberation. Research on group decision making shows that small teams of diverse experts often outperform individuals, provided they avoid conformity pressures. With five members, communication is still manageable. Each voice can be heard. Coordination costs rise modestly but remain within reason.

The challenges include negotiation and possible deadlock. Conflicts emerge between functional logics: finance may prioritize return on investment, while R&D may push for strategic innovation. The group must adopt clear decision rules—consensus, majority, or CEO tiebreaker. Without them, stalemates are likely. Groupthink is also a risk if cohesion is too strong, though in practice functional diversity often counteracts this.

This model strikes a balance. It slows decisions somewhat compared to the CEO-only case but gains legitimacy and richer information processing. Empirical studies suggest that groups of 5–9 members are close to optimal for complex strategic tasks.

Case 3: Twenty Senior Executives

When the circle expands to around twenty executives and VPs, the character of decision making changes again. The group is large enough that direct deliberation becomes difficult. Meetings risk devolving into speeches rather than discussions.

The advantages include greater representation and broader expertise. More functions and business units have a voice. This enhances legitimacy: managers see that their perspectives are included. The information base is wider, capturing local market knowledge and operational insights.

The problems, however, multiply. Coordination costs rise steeply—simply scheduling discussions becomes a burden. Information overload is real: twenty executives cannot each engage deeply with dozens of proposals. Free-riding appears, as individuals rely on others to do the hard work of reviewing. Coalitions emerge, with executives aligning along functional or divisional lines. Preference aggregation becomes difficult: the probability of deadlock or unstable compromise increases.

To cope, the process requires formal structures. Proposals must be pre-screened by a committee. Deliberation may be organized in subgroups that report back. Voting rules—majority, supermajority, weighted by role—must be specified. Facilitation becomes essential to prevent dominance by a few forceful voices.

The trade-off is clear: legitimacy and diversity rise, but speed and efficiency fall. The process risks paralysis unless carefully designed.

Case 4: One Hundred Leaders

Finally, imagine the firm giving equal decision rights to all 20 executives and 80 directors—a 100-person assembly. This might be the corporate analogue of a parliament.

The benefits are inclusiveness and legitimacy. Many, perhaps all senior leaders are represented. Decisions carry broad internal support, reducing resistance to implementation. The information base is as wide as the organization itself. Symbolically, the process signals fairness and transparency.

But the costs are severe. Coordination becomes overwhelming. Large meetings become theater rather than deliberation. No one can process all the information, and most participants disengage. Free-riding is rampant; individuals know their voice is marginal. Coalitions form, politics dominates, and conflict intensifies. Preference aggregation is intractable without formal voting mechanisms—ranked ballots, digital platforms, perhaps even secret votes.

Decision speed collapses. What could be done in days by a CEO or weeks by a small team now stretches into months. The assembly model might best be suited to ratification or consultation, not to direct investment choice. Like legislatures, it may function to legitimate and oversee, but actual agenda setting and filtering must occur elsewhere.

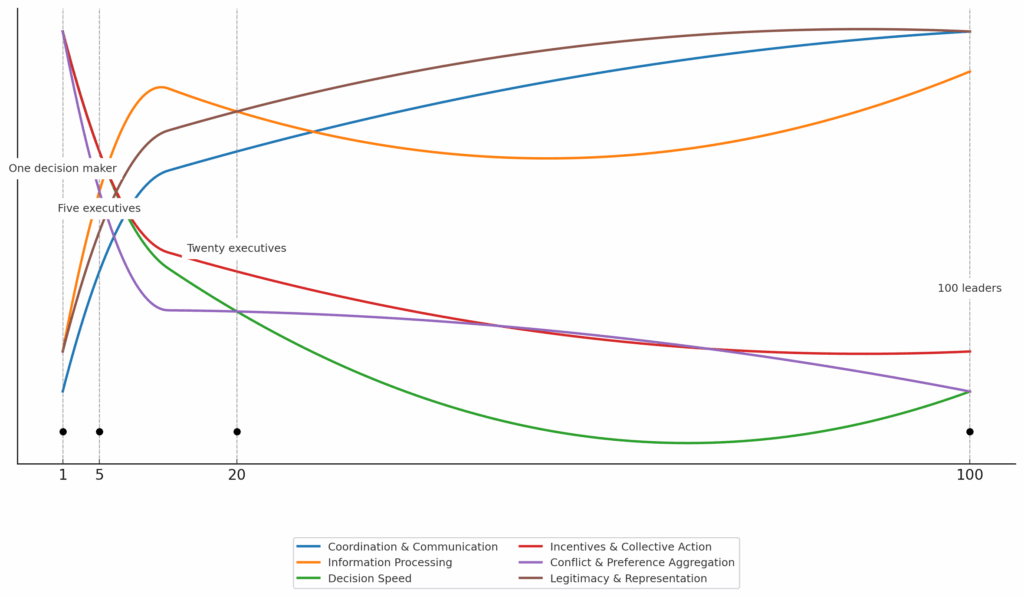

Cross-Case Comparison

Looking across the four cases suggests that each scale brings distinct strengths and weaknesses, shown in relative terms in the table.

| Criterion | One Decision Maker | Five Executives | Twenty Executives | 100 Leaders |

|---|---|---|---|---|

| Coordination & Communication | Very low | Moderate | High | Extremely high |

| Information Processing | Low | Medium | High (risk of overload) | Very high in principle, but unmanageable |

| Decision Speed & Efficiency | Very high | Moderate | Low | Very low |

| Incentives & Collective Action | Clear accountability | Some shirking, functional bias | Free-riding, coalitions | Severe free-riding, politics dominate |

| Conflict & Preference Aggregation | Absent | Negotiated, manageable | Risk of deadlock/coalitions | Very difficult; requires formal voting |

| Legitimacy & Representation | Low | Moderate | High | Very high |

| Optimal Group Size Trade-offs | Best for speed, consistency | Near-optimal for balance | Beyond optimal, needs structure | Far beyond optimal; best for ratification |

The Core Trade-offs

Several themes emerge.

- Speed versus inclusiveness. Smaller groups act faster, larger groups confer legitimacy. Firms must decide whether rapid responsiveness or broad buy-in is more valuable in their environment.

- Information diversity versus overload. Larger groups possess more knowledge but also face limits to integration. Effective processes require filtering and summarizing information to avoid paralysis.

- Accountability versus diffusion. In small groups, responsibility is clear; in large groups, it dilutes, increasing free-riding and politics.

- Conflict management. Conflict is absent in the single decision maker model but grows rapidly with group size. Formal rules for aggregation—voting, weighted representation, delegated committees—are unavoidable beyond a handful of members.

- Legitimacy. Larger groups enjoy more legitimacy, both because they represent more voices and because procedures appear fairer. But legitimacy can evaporate if the process becomes symbolic or ineffectual.

The following chart summarizes the tradeoffs.

Which Model Should Firms Choose

There is no universal answer. The optimal design depends on the firm’s environment, culture, and priorities. Three stylized recommendations follow.

- Dynamic markets with high uncertainty: Favor smaller groups (Cases 1 or 2). Speed and decisive action matter most. Legitimacy risks can be managed through strong communication and post-hoc justification.

- Stable industries with complex stakeholder interests: Mid-sized groups (Case 3) may be optimal. Legitimacy and information diversity outweigh speed. Governance structures must be in place to manage conflict.

- Firms seeking symbolic inclusiveness: Large assemblies (Case 4) can serve a ratifying role, enhancing legitimacy and transparency, but should not be relied upon for actual investment selection. Pre-screening by smaller expert committees is essential.

In practice, many firms adopt hybrid models. A small executive committee filters and prioritizes proposals. Broader senior management is consulted for input and legitimacy. The CEO retains a final say. The large group endorses or ratifies decisions, lending legitimacy. Each layer plays a distinct role, balancing speed, diversity, and legitimacy.

Conclusion

The case of new product investments illustrates a general principle: decision process design must be tailored to group size. What works for one person or five people cannot simply be scaled up to twenty or one hundred. As groups grow, coordination costs, collective action problems, and conflicts rise sharply. Formal structures become indispensable.

At the same time, larger groups confer legitimacy, which can be vital for implementation. Employees are more likely to support decisions they feel represented in, even if their own proposal is not chosen.

Governance design needs to balance these trade-offs. Firms must decide how much speed to sacrifice for inclusiveness, how much accountability to trade for legitimacy, and how to structure information flows so that diversity enhances rather than overwhelms.

References

- Arrow, K. (1951). Social Choice and Individual Values. Yale University Press.

- Hackman, J. R. (2002). Leading Teams. Harvard Business School Press.

- Hong, L., & Page, S. (2004). “Groups of diverse problem solvers can outperform groups of high-ability problem solvers.” PNAS, 101(46), 16385–16389.

- Janis, I. L. (1982). Groupthink. Houghton Mifflin.

- Kahneman, D. (2011). Thinking, Fast and Slow. Farrar, Straus and Giroux.